Execution Algorithms in Crypto Market Making

6 minutes

6 minutes

Crypto markets have matured into deep, 24/7 venues, attracting institutional players who demand efficient trade execution. Even small inefficiencies can erode performance, for example, a mere 0.073% slippage on each trade can compound into a 26.65% drag on returns over a year. To combat this, institutions and liquidity providers are increasingly leveraging algorithmic execution strategies, from TWAP and VWAP to percentage-of-volume participation and smart order routing, to minimise slippage and market impact.

The Liquidity Challenge on CEXs

Liquidity is the oxygen of active trading, and crypto liquidity varies widely across venues and pairs. Top-tier exchanges (e.g. Binance, Coinbase, OKX) routinely handle enormous volumes, BTC/USD or BTC/USDT markets can see >$20 billion traded daily, resulting in extremely tight spreads and minimal slippage. For instance, during peak hours on major exchanges, a $1 million market order in BTC might move the price by less than 0.05% (just 5 basis points). In contrast, less liquid pairs or venues tell a different story: niche altcoin pairs or fiat crosses can have shallow order books where spreads balloon past 1% and a relatively small order can “choke” the market. As one analysis put it, “deep books on BTC-USDT fill quickly; niche micro-caps can slip fast.”

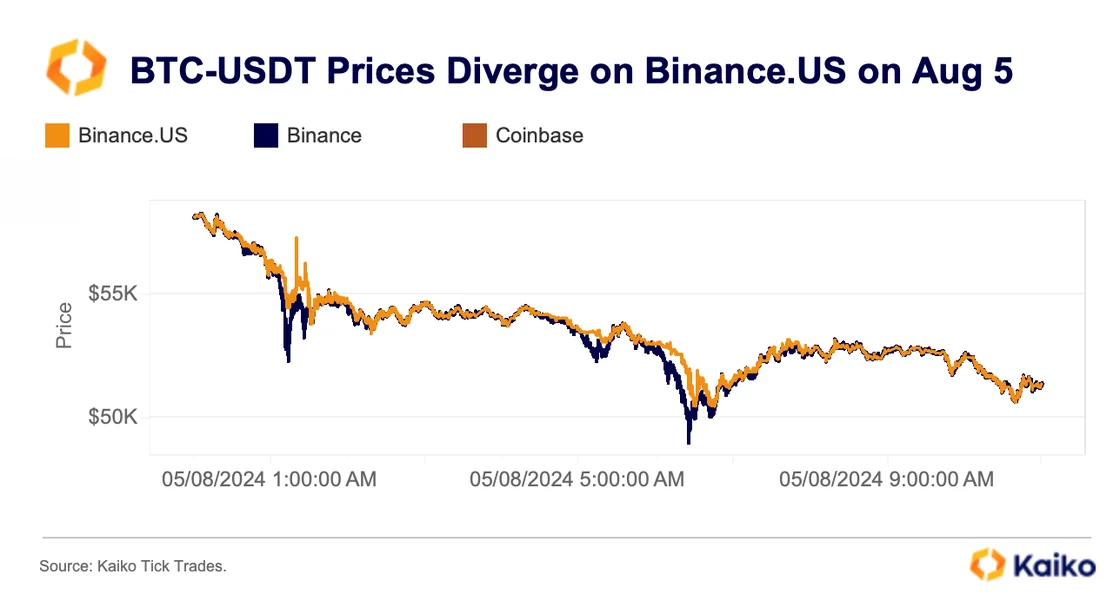

Slippage, the difference between the expected price and execution price, is the key metric to watch. It stays low in deep markets but spikes when liquidity thins out. A recent stress test on August 5, 2024, illustrates this starkly. In a sharp sell-off, Bitcoin prices on a smaller exchange (KuCoin’s BTC-EUR) diverged dramatically, with a $100k sell order experiencing over 5% slippage on that illiquid pair. Even usually-liquid markets felt a pinch: some top stablecoin-quoted books saw slippage jump >3 basis points under duress. By contrast, major USD or USDT markets absorbed the same sell-off with only a few bps of impact. Figure 1 below shows how much slippage varied across exchanges that day, from negligible on the biggest platforms to several percent on smaller ones.

Figure 1: Hourly price slippage on Aug 5, 2024 (sell-off day); blue lines show the lowest slippage and orange dots show the peak slippage for a $100k BTC sell order on various exchange pairs. Less liquid markets like KuCoin’s BTC/EUR saw >5% price impact at the worst moment, while deep markets like Binance’s BTC/USDT stayed below 0.05%. (Data source: Kaiko)

This variability means execution strategy is critical. A large order dropped in a shallow market can sweep multiple order book levels, incurring high cost. For example, Coinbase’s BTC/EUR pair is notably less liquid than its BTC/USD pair, which led to outsized volatility and price gaps in a high-stress scenario as the order book depth simply evaporated. Smart traders and market makers counter this by choosing the right venues and algorithms: either seek deeper liquidity pools or slice the order intelligently to avoid tipping the market. Notably, liquidity also fluctuates with time. Crypto’s 24/7 cycle exhibits thinner books on weekends and off-peak hours. Depth is increasingly concentrated during weekdays, so an algorithm might need to slow down overnight. In sum, the playing field is uneven: knowing where and how to execute can mean the difference between a 1-2 bps slippage and a 100+ bps rout on a large trade.

CEX vs DEX: Brief Execution Contrasts

On centralised exchanges (CEXs), the presence of a full order book allows for sophisticated order types and algorithmic execution. Traders can see bid/ask depth and use strategies like posting hidden iceberg orders or slicing flows over time. In contrast, decentralised exchanges (DEXs) often use automated market maker (AMM) models where liquidity is a curve, slippage is predetermined by pool size and the AMM formula. Large market orders on a DEX can face immediate price impact (slippage) due to this formulaic liquidity. While execution algos per se are less common within a single AMM pool, aggregators serve a similar role: a DEX aggregator (e.g. 1inch or Matcha) will split a large swap across multiple DEX pools to minimise price impact, effectively a form of smart order routing. The concept is analogous to CEX execution algorithms: both aim to break up orders and tap multiple liquidity sources to get the best price. However, this post will focus on CEX scenarios, where institutions and exchange operators have the most flexibility to deploy custom execution algorithms (and where most fiat-quoted pairs like BTC/USD, ETH/USDT, SOL/EUR are traded with order books).

Algorithmic Execution Strategies on Crypto Exchanges

Modern crypto trading desks use a toolkit of algorithmic execution strategies to improve fill quality and reduce market impact. The right algorithm (or combination) depends on the asset’s liquidity profile, the size and urgency of the order, and market conditions. Below, we outline key algorithm types: TWAP, VWAP, POV and Smart Order Routing, explaining how each works and when to use them, with data-driven insights on their performance.

TWAP: Time-Weighted Average Price

TWAP splits an order into equal (or proportional) parts over a specified time interval, aiming for the average price over that period. For example, an algorithm might execute 1/60th of a large order every minute for an hour. TWAP cares only about time, not volume, so it maintains a steady pace regardless of market activity. This makes it ideal for discreet accumulation or distribution when you want to minimise detection and avoid chasing volume. If you have a large sell to do over a day with no particular rush, TWAP will ensure you “place a series of small orders across the day” at a consistent pace. A big advantage is that TWAP won’t suddenly speed up in thin markets; in fact, during low-volume periods (like overnight sessions or weekends), a time-based approach stays gentle: VWAP might struggle for data in these hours, whereas “TWAP remains relatively stable since it just divides time equally, irrespective of volume levels. This helps keep your presence under the radar in illiquid windows.

Cost savings: A well-designed TWAP algorithm can significantly reduce costs by posting orders passively (as a maker) instead of crossing the bid-ask spread. Industry data shows this clearly. For instance, Talos reported that using its TWAP algo (which intelligently posts limit orders) saved on the order of 2–10 basis points in execution costs compared to a naive approach. How? The TWAP algorithm avoids paying taker fees and wide spreads whenever possible. In fact, for moderate-sized trades (~5–10% of market volume over the execution window), Talos achieved a median ~88% fill rate as maker (only ~12% of child orders had to take liquidity), whereas an impatient algorithm would cross the spread much more often. With maker fees often 10 bps lower than taker fees on exchanges, this high passive fill rate translates into major fee savings. Talos calculated that on a $10 million parent order representing 5–10% of the market’s volume, their TWAP saved roughly $8,800 in fees versus a spread-crossing execution. And that’s before considering price impact; by not sweeping the order book, TWAP also avoids pushing the price against you as much. Another crypto trading firm similarly saw about 74% of its order flow executed passively (as maker) when using algorithmic execution in late 2023, indicating considerable cost savings for their clients.

Use cases: TWAP is favoured when time is on your side. If an institution wants to buy, say 10,000 SOL over a day without spooking the market, a TWAP can drip the orders out evenly. It’s simple, predictable, and ensures you “buy or sell at a pace aligned with time, not volume surges.” Traders often choose TWAP for extended timeframes or illiquid trading hours, essentially anytime you want to minimise impact and don’t mind some execution duration. Do note that TWAP doesn’t react to market conditions; if a big price move happens during your schedule, a pure TWAP will keep trading through it. (Some advanced TWAP implementations have guardrails to pause in volatile spikes.) Overall, TWAP shines for stability and stealth, at the cost of potentially missing opportunities during volume spikes (since it won’t front-load even if liquidity suddenly improves).

VWAP: Volume-Weighted Average Price

VWAP algos pace their execution in proportion to trading volume. Instead of equal time slices, VWAP tracks the market’s volume curve, executing more aggressively during high-volume intervals and easing off during lulls. The goal is to match (or beat) the day’s VWAP benchmark, essentially getting an average price in line with the market’s overall liquidity-weighted price. Traders often use VWAP as a benchmark to judge execution quality, and many institutions aim to “do no worse than VWAP” for large orders. In practice, a VWAP algo will observe the historical or real-time volume profile (e.g. if 2pm to 3pm tends to have 10% of the day’s volume, the algo will try to do ~10% of the order in that hour). This means heavy trading when everyone else is trading (to hide in the crowd) and holding back when volumes are thin.

Use cases: VWAP is ideal for large orders in highly liquid markets, especially when you want to hide large trades among heavy volume. If you’re trading a major pair like BTC/USDT during peak market hours, a VWAP strategy helps you blend in with the flow; your activity is a drop in the bucket of the crowd. Because VWAP dynamically adjusts to volume, it can minimise market impact when liquidity is plentiful (you trade more when the market can absorb it). Institutions favour VWAP when they have a volume target: e.g. “get me this position but make sure I participate no more than 15% of the volume.” In fact, a Percentage-of-Volume (POV) algorithm is a close cousin of VWAP. Instead of a pre-set volume curve, POV simply says “execute x% of the market’s volume until done.” This ensures you never outpace the market. For instance, a POV of 10% will mean that if the market trades 1000 units in a minute, you trade 100 units in that minute. It’s a dynamic throttle that is very useful in fast-moving or unpredictable conditions: if volume dies off, your trading slows (preventing outsized impact), and if volume surges, you automatically increase your pace to get the order done quicker.

Performance: A well-tuned VWAP or POV algo can often beat a time-based execution when volume patterns are favourable. In traditional markets, algo providers expect only a slight slippage versus VWAP (often on the order of 1 – 2 bps for large orders), and crypto markets are moving in that direction as liquidity improves. The key is that by matching execution to available liquidity, VWAP/POV minimize the market impact component of cost. However, one must be cautious in low-volume periods; a pure VWAP might leave you under-filled if volume unexpectedly dries up. Traders solve this by either mixing VWAP with a time-based component or falling back to TWAP in off-peak hours. The choice between VWAP and TWAP often “depends on liquidity conditions and your goal”: if volumes are robust and you want to mask your trade among the crowd, VWAP (or POV) is preferred; if volumes are uncertain or you value a consistent pace, TWAP is the ally. Many execution platforms let you set a participation cap (e.g. never more than 20% of volume) on a VWAP order, effectively blending the concepts. This ensures the algo won’t go wild in a sudden volume vacuum or spike. Remember, if you push VWAP/POV to too high a participation rate, you defeat the purpose by becoming the dominant player and impacting the price; studies show that price impact rises significantly with higher participation rates (and shorter execution horizons). In other words, aggressiveness has a cost: trying to be 50% of the market’s volume will likely drive up slippage dramatically, whereas staying around 5-10% of volume often keeps slippage within a few basis points.

Implementation Shortfall (Arrival Price) Strategies

While TWAP and VWAP are schedule-based, Implementation Shortfall (IS) algorithms take a more dynamic approach. The implementation shortfall is the difference between the price when you decide to trade (arrival price) and the final execution price. IS algos actively balance market impact vs. timing risk to minimise that shortfall. They will trade faster when getting the order done seems prudent (e.g. price moving favourably or low liquidity expected later) and slow down if the market is calm or moving against the trade. In essence, IS algos incorporate a “urgency” or risk-aversion parameter, how much you’re willing to pay in impact to reduce the risk of the price running away. This framework directly tackles the Trader’s Dilemma: the longer you take to execute, the less immediate impact you impose, but the more you risk the market moving before you finish (adverse selection). A very urgent (high-aggression) setting means the algo leans toward taking liquidity to complete quickly (accepting higher market impact), whereas a low-urgency setting means it will work the order patiently and try to be mostly passive, tolerating more time risk. The optimal point often lies in between. Advanced crypto trading desks have started to adopt these IS strategies, especially for large institutional orders, as they mimic the decision-making a skilled trader would do: adjust on the fly based on real-time order book info, volatility, and progress towards completion.

Use cases: An IS or arrival-price strategy is useful when market conditions are uncertain, and you need to dynamically adjust. For example, if an institution must unload a large position in an altcoin over a few hours, a static TWAP might be too blunt; an IS algo can slow down if the market is sliding (to avoid dumping into a falling market) or speed up if a big buyer appears (taking advantage of the liquidity). Exchange operators looking to attract institutions may consider offering IS-type algos or TCA (transaction cost analysis) tools, since sophisticated players will want to optimise that shortfall metric. While concrete stats on crypto implementation shortfall performance are proprietary, the goal is to beat simpler benchmarks. Notably, one crypto execution provider reported an average arrival slippage of -0.58 bps (i.e. just half a basis point of shortfall) on its flow, an extremely low number that suggests their dynamic execution and high passive fill rates are paying off. In comparison, traditional equity brokers often see 10-15 bps arrival slippage on large orders. This indicates that crypto markets, with the right algos, can achieve excellent execution quality, likely due to the combination of deep liquidity in top venues and 24/7 opportunities to work an order. The takeaway: adaptive execution (whether via an explicit IS algo or a well-tuned POV with dynamic adjustments) can squeeze out extra bps of performance, which is crucial for institutions trading size.

Smart Order Routing (SOR)

Smart Order Routing isn’t about when or how fast to trade, but rather where to execute. The crypto market is highly fragmented, liquidity for BTC or ETH is split across dozens of exchanges globally, and fiat pairs like BTC/USD, ETH/USDT, SOL/EUR might each trade on several venues with different order book depths. No single exchange has a monopoly on liquidity. In fact, the top 10 exchanges by volume only account for roughly half of all trading, with the rest scattered across hundreds of smaller venues. This means the best price for your order may not be on the exchange you’re currently using; it could be a few dollars better on another venue. SOR systems solve this by aggregating and routing orders across multiple exchanges to ensure best execution. Essentially, an SOR will check prices and available depth on all connected venues and either sweep the best bids/offers simultaneously or intelligently split the order to where liquidity is richest. For example, if you want to sell 100 BTC, an SOR might simultaneously sell 50 on Exchange A (deepest buyer interest), 30 on Exchange B, and 20 on Exchange C to get the best average price, instead of dumping all 100 on one exchange and pushing its price down.

Performance impact: The benefits of SOR are strongly evidenced by data. Analytics from 2023 show that firms using multi-venue execution significantly outperform single-venue traders. One analysis found that a $1 million BTC market order would incur an extra 4-13 bps of slippage if executed on a single exchange versus being smart-routed across four exchanges (median case). For a $5 million BTC order, the slippage penalty on one venue jumped to about 134 bps (1.34%) in the median scenario. In other words, a large trade could lose over 1% of value just by not spreading it out! Even for more modest trades, the savings are real: “Even a $1M BTC trade can save on the order of 5–10 bps via multi-venue execution, while a $5M trade might save over 1% in price slippage.”. The effect is exponential for illiquid assets: the same study saw certain altcoin orders that would have 70% (!) price impact on a single tiny exchange, whereas a multi-venue approach reduced that dramatically. Clearly, smart routing turns fragmentation from a weakness into an advantage – by accessing pockets of liquidity everywhere, you avoid leaving money on the table or crashing one order book. An SOR would simply avoid the thin venue except for maybe a small portion, directing most of the flow to where depth is better.

Beyond just better prices, SOR offers qualitative benefits. It reduces the chance of information leakage and front-running because your large order is disguised across venues. No single order book sees the full size, so other traders are less likely to react adversely. It also provides redundancy: if one exchange goes down or into maintenance (not uncommon), you can reroute to others and keep trading. For exchange operators, offering SOR (or connecting to liquidity networks) can attract institutional flow by assuring them that their orders will find the global best price, not just the local best. A recent example is Nubank (a major fintech bank in Brazil) integrating an SOR engine in 2023 so that its crypto trading app sources liquidity both locally and overseas, giving users “more competitive prices securely and reliably” in BRL markets. The result is tighter spreads and lower costs for end-users, which is a win-win for the platform’s reputation and the traders’ P&L.

Improving Execution Quality: Strategy and Insights

Execution algorithms are more than just technical tools; they are strategic levers for institutions and liquidity providers. By tailoring execution methods to an asset’s liquidity profile and the trader’s objectives, significant improvements in outcome can be achieved:

- Reduce Slippage and Market Impact: The primary goal of all these algos (TWAP, VWAP, POV, IS, SOR) is to minimise slippage. A crypto fund or market maker that consistently saves even 5–10 bps on trades is gaining a serious edge. Those basis points directly translate to P&L, or better prices that can be passed on to clients. For liquidity providers, using algos to offload inventory gradually means they can quote tighter spreads in the market (since they’re less afraid of getting stuck with a large position they can’t unwind cheaply). This improves overall market quality. As shown, a thoughtful execution strategy can turn what would have been a 20 bps cost into maybe a 5 bps cost, which over many trades adds up to massive savings.

- Match Algorithm to Market Conditions: There is no one-size-fits-all; savvy traders combine algorithms or adjust parameters on the fly. For example, an institution might start a day using VWAP in the morning when volumes are high, then switch to a slower TWAP in the afternoon if things quiet down, and finally use an Implementation Shortfall approach near the close to manage any residual risk as they finish the order. The “trader’s dilemma” of impact vs. risk is ever-present; the right algos help find that balance automatically. If urgency is high (say, news is coming), you dial up participation or use aggressive IS; if you have more time, you dial it down. Always monitor execution with transaction cost analysis (TCA), compare your fills to benchmarks like VWAP or arrival price. Continuous TCA feedback allows fine-tuning of algorithms to further cut costs.

- Leverage Venue Analytics: Different exchanges have different “personalities.” Some have deeper order books in USD, others in USDT; some have better liquidity during Asian hours vs US hours. Institutions should route orders to venues that play to these strengths. For instance, BTC/EUR might trade best on a European exchange like Bitstamp or Kraken with solid EUR banking, whereas SOL/EUR could be so illiquid that it’s better to trade SOL/USD and do a separate USD to EUR FX conversion. Know the typical liquidity profile of your venues: if an exchange’s BTC/USD depth is 5x stronger than its BTC/EUR, it might be wise to execute via the USD pair and convert currency separately. Key venues like Binance or OKX often offer the tightest spreads for stablecoin-quoted pairs, while Coinbase, Kraken, and Bitstamp lead in fiat pairs like USD or EUR, and these differences matter when choosing an execution plan. Use algos that can source liquidity from multiple books (via SOR) or at least pick the right time to trade on a given venue (some exchanges have predictable liquidity spikes at certain hours).

In conclusion, institutions and exchange operators can greatly enhance execution quality by deploying the right algorithms. Crypto markets may be volatile and fragmented, but that is as much an opportunity as it is a challenge. By slicing orders intelligently in time (TWAP/VWAP), proportional to volume (POV), and across venues (SOR), large trades can be executed with minimal footprint, often just a few basis points off the theoretical best price. The data shows tangible benefits: lower slippage, lower fees and better average prices achieved. For an exchange operator, providing these algorithmic tools (or connectivity to liquidity networks) can attract sophisticated traders who demand best execution. For liquidity providers and market makers, algos are indispensable for managing inventory and risk without roiling the market. In a world where every basis point counts once trade sizes grow into the six or seven figures, execution algorithms have become a critical part of the crypto trading stack. Execution is king, and in crypto’s arena, the best algorithms are helping traders win with precision and data-driven confidence.

Further Readings:

- Amberdata Blog: Comparing Global VWAP and TWAP for Better Trade Execution:

blog.amberdata.io - Anboto Labs (Medium): Slippage, Benchmarks and TCA in Crypto Trading:

medium.com - CryptoSlate: Crypto Exchanges vs. Brokers: Liquidity and Execution Quality

cryptoslate.com - Kaiko Research: Liquidity Fragmentation and Price Slippage Analysis (2024)

research.kaiko.com

Contact Us

We are always open to discussing new ideas. Do reach out if you are an exchange or a project looking for liquidity; an algorithmic trader or a software developer looking to improve the markets with us or just have a great idea you can’t wait to share with us!