The GENIUS Act & the New Era of Stablecoin Liquidity

8 minutes

8 minutes

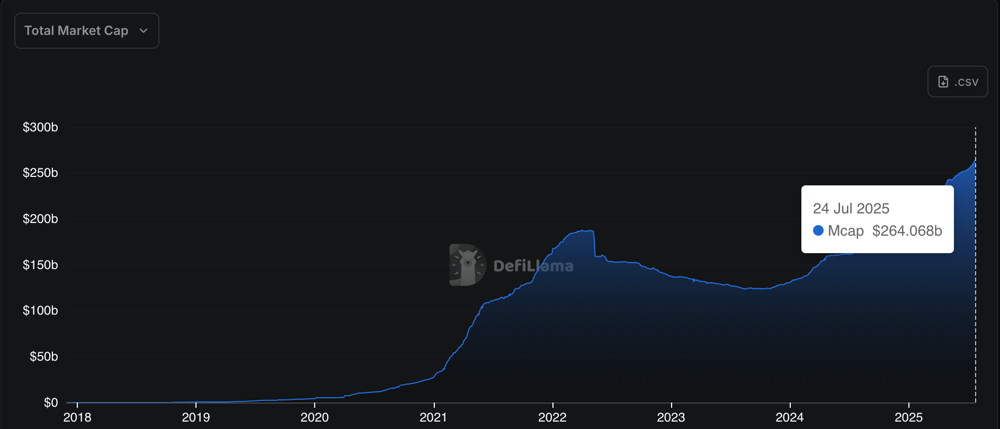

As of July 2025, the stablecoin market is roughly $270 billion, underscoring how crucial these dollar-pegged tokens have become for crypto liquidity. Stablecoins facilitate an estimated 60%+ of crypto trade volume, serving as the lifeblood of decentralized finance (DeFi) and exchanges. Now, a landmark US bill; the Guiding and Establishing National Innovation for US Stablecoins Act of 2025 (GENIUS Act), promises to reshape this landscape. Enacted in July 2025 with broad bipartisan support, the GENIUS Act is the first federal law to comprehensively regulate “payment stablecoins,” ushering in a new era of regulatory clarity and confidence for digital dollars. In this post, we analyze the Act’s scope and potential impacts on stablecoin liquidity across different models (fiat-backed, algorithmic and crypto-collateralized). We also explore how market makers, the liquidity providers in crypto markets, might adapt under this legislation, and what it means for US and global markets.

(Note: This neutral analysis is published on Gravity Team’s blog to inform a technical audience of traders and developers.)

Overview of the GENIUS Act

Background: Introduced by a bipartisan group of US Senators in early 2025, the GENIUS Act establishes a regulatory framework for payment stablecoins, i.e. digital assets designed to maintain a stable value relative to a fiat currency (typically the dollar) and redeemable on demand at par. The Act was signed into law in July 2025, following a 68–30 Senate vote and a 308–122 House vote, making it the first major crypto legislation enacted in the US. Its core aim is to integrate stablecoins into the traditional financial regulatory perimeter without stifling innovation. Below is an overview of key provisions:

- Permitted Issuers Only: The Act prohibits anyone other than a “permitted payment stablecoin issuer” from issuing a payment stablecoin to U.S. users. In practice, this limits issuance to regulated entities:

- Bank Subsidiaries: A subsidiary of an insured depository institution (e.g. a bank’s affiliate) can issue stablecoins with approval from its federal banking regulator.

- New OCC Charter: A federal qualified nonbank stablecoin issuer can be chartered by the Office of the Comptroller of the Currency (OCC) (including fintech firms or even uninsured national banks) to issue stablecoins under OCC supervision.

- State-Qualified Issuers: Nonbanks can also pursue a state license in a state that establishes a “substantially similar” regulatory regime. However, any state-approved issuer exceeding $10 billion in stablecoin circulation must come under federal oversight (OCC or Fed) unless a special waiver is granted.

- Full Reserve Backing: All permitted stablecoins must be 100% backed by high-quality liquid assets on a one-to-one basis. Eligible reserves include U.S. dollars, demand deposits at insured banks, short-term U.S. Treasuries, Treasury repo agreements, certain money market funds, or tokenised forms of these assets. This mandate ensures that each stablecoin is effectively a redeemable IOU for $1 of real assets, guarding against runs. Issuers must publicly disclose their redemption policies and publish detailed monthly reserve reports audited by a registered accounting firm.

- Regulatory Oversight: Permitted issuers will face bank-like supervision. Federal stablecoin issuers answer to the OCC, while bank-affiliated issuers are overseen by their primary federal regulator (e.g. Federal Reserve or FDIC). State-level issuers remain under state oversight unless they grow large (>$10B) or their state’s rules fall short of the federal standard. Importantly, the Act explicitly clarifies that a compliant payment stablecoin “is not a security or commodity” under U.S. law. This provides long-sought clarity: bona fide stablecoins will not be treated as stocks or ETFs by the SEC, removing a major regulatory uncertainty.

- Business Restrictions: The Act confines what stablecoin issuers can do, aiming to minimise risk. Issuers may only engage in issuing and redeeming stablecoins, managing their reserves, providing custodial wallet services, and other incidental activities directly supporting these functions. Unlike banks, they generally cannot lend or use reserves for other businesses (with strict limits on any re-use of reserves). This narrow scope protects the reserves from being diverted into risky investments. Moreover, issuers must not advertise stablecoins as “FDIC-insured” (since stablecoin holdings are not deposits insured by the government).

- No Interest to Holders: To prevent stablecoins from behaving like bank deposits, the Act bans issuers from paying any interest, dividends, or yield to stablecoin holders. In other words, you cannot earn interest simply by holding a regulated stablecoin in your wallet. This prohibition closes the door to programs like the failed Terra/Anchor protocol (which enticed users with ~20% APY on an algorithmic stablecoin), and it alleviates regulators’ concerns that stablecoins might compete with bank savings accounts. Any “reward” or financial incentive for holding a stablecoin is disallowed, ensuring these tokens function purely as payment instruments and not as investment products.

- AML & Risk Controls: Permitted stablecoin issuers are deemed “financial institutions” under the Bank Secrecy Act, bringing them under full anti-money-laundering (AML) and Know-Your-Customer requirements. Issuers must implement KYC onboarding, monitor transactions for illicit activity, file suspicious activity reports (SARs), and comply with OFAC sanctions screening. They also need technological capability to freeze or seize stablecoins subject to lawful orders, meaning the smart contracts for these coins will include blacklisting functions to block illicit addresses. In sum, stablecoin networks will no longer operate in a compliance grey zone; they are expected to meet the same financial crime standards as traditional payment networks. The Act even calls for studies on detecting illicit finance in stablecoins and DeFi, foreshadowing further guidelines in the next few years.

- Foreign Issuers: The GENIUS Act doesn’t ignore the global nature of crypto. A foreign stablecoin issuer (e.g. an overseas company like Tether) may only offer its stablecoin to U.S. customers if (a) the Treasury Secretary deems the issuer’s home country regulatory regime “comparable” to U.S. standards, (b) the issuer registers with the OCC and consents to U.S. oversight, (c) it maintains sufficient U.S.-held reserves for U.S. users, and (d) its home country is not under U.S. sanctions or identified as a money-laundering haven. This is a high bar. Practically, it means unregulated foreign stablecoins will be barred from the U.S. market. Absent compliance, such coins “shall not be treated as cash or cash equivalent” by U.S. institutions; they can’t be used as accepted payment or as margin/collateral in regulated trading venues. This puts the onus on major offshore stablecoins to either seek compliance or lose access to U.S. customers.

Impact on Different Types of Stablecoins

The new law’s impact will not be uniform across all stablecoin models. It creates clear winners (fully-backed, compliant stablecoins) and challenges for others (algorithmic or decentralised tokens). Below, we examine implications for the major categories of stablecoins:

- Fiat-Backed Stablecoins (e.g. USDC, USDT): Fiat-backed stablecoins, those backed by cash and equivalents, are the primary target of the GENIUS Act. Going forward, only fiat-backed coins issued by licensed entities with one-to-one reserves will be legally viable in U.S. markets.

This is likely to benefit U.S.-regulated stablecoins like USD Coin (USDC), which already emphasise reserves and transparency. Circle (issuer of USDC) has signalled support for federal oversight and could seek a national charter or Fed supervision to become a permitted issuer. Banks and traditional financial institutions are entering the fray as well. With regulatory clarity in place, major banks and asset managers have announced plans to issue their dollar stablecoins compliant with the Act’s standards.

For example, Bank of America, JPMorgan and Citigroup all indicated they are exploring or preparing stablecoin offerings shortly after the bill’s passage. This influx of new, regulated stablecoins could increase overall fiat-backed stablecoin supply and competition, potentially tightening spreads and boosting liquidity on exchanges. On the other hand, the Act poses a strategic dilemma for Tether’s USDT, the largest stablecoin globally. Tether, now based in El Salvador, does not presently meet the Act’s stringent requirements (full transparent reserves, U.S. oversight, etc.). Legal experts suggest Tether may choose not to attempt US compliance, instead continuing to focus on non-US markets where its coin is widely used. US exchanges and brokers, however, would likely be discouraged (or even prohibited) from offering USDT trading pairs once the law is implemented. We may see a liquidity bifurcation: USDC and bank-issued coins gain dominant US market share, while USDT (and similar foreign stablecoins) remain liquid on offshore platforms and in emerging markets. In the long run, if US standards become globally recognised (or if Tether pursues a compliant US affiliate coin as hinted by its CTO), this gap could narrow. In the near term, though, fiat stablecoin liquidity will consolidate around those issuers willing and able to meet rigorous U.S. regulatory criteria. - Algorithmic Stablecoins: Algorithmic stablecoins, those that attempt to hold a peg via algorithms or seigniorage mechanisms rather than hard collateral, are effectively sidelined under the GENIUS Act. The Act’s definition of “payment stablecoin” requires an issuer who “is obligated to redeem” the token for a fixed monetary amount, implicitly excluding typical algorithmic designs where no centralised issuer guarantees redemption. Moreover, US regulators have strongly criticised algorithmic stablecoins after the collapse of TerraUSD (UST) in 2022, which erased ~$18 billion in value and briefly sent shockwaves through crypto markets. In response, the new law focuses on fully reserved models and explicitly plans a “separate treatment” for algorithmic stablecoins in the future. In practical terms, this means algorithmic stablecoins cannot be issued or marketed in the US as payment stablecoins. They will not qualify as regulated stablecoins and thus will be shunned by compliant exchanges and institutions. Algorithmic projects (if any persist after Terra’s failure) will be relegated to experimental DeFi niches outside US jurisdiction. It’s worth noting that even before the Act, purely algorithmic USD stablecoins had largely fallen out of favor due to their inherent fragility. The GENIUS Act cements this reality: unbacked algorithmic tokens have no place in the mainstream US market. We can expect any future innovation in this area to be met with heavy scrutiny or outright prohibition unless and until a truly robust design emerges (a high bar, given past evidence).

- Crypto-Collateralized Stablecoins (e.g. DAI): Crypto-backed stablecoins, such as MakerDAO’s DAI, are a special case. They are backed by assets (cryptocurrency collateral rather than cash), and often over-collateralized, but they have decentralized issuers (protocols or DAOs rather than regulated companies). DAI, for instance, is generated by a smart contract system that accepts crypto assets (ETH, BTC, etc.) as collateral and has a current market cap around $4+ billion. Under the GENIUS Act, DAI does not neatly fit the definition of a permitted stablecoin, since there is no single legal entity “issuer” that can register with regulators. Unless MakerDAO significantly reorganizes (for example, by establishing a regulated trust entity to issue DAI), DAI would likely be deemed an unpermitted stablecoin in the US. This has several implications: US-regulated exchanges might delist or avoid DAI trading, and DAI would not be recognized as “cash equivalent” or acceptable collateral under US financial rules. In essence, DAI and similar decentralized stablecoins could face a barrier to US adoption. MakerDAO has already taken steps that hint at seeking compliance, for instance, backing a sizable portion of DAI with real-world assets like short-term Treasuries via partner banks.

However, meeting the Act’s full requirements would likely require bringing the project under direct regulatory supervision, potentially compromising its decentralized nature. This is a tension many DeFi projects will grapple with. The Act may push crypto-collateralized stablecoins to evolve: we might see hybrid approaches where a regulated entity issues a stablecoin that is partially backed by crypto (with appropriate haircuts and controls) to marry the transparency of on-chain collateral with the legal safeguards of a permitted issuer. If not, the role of DAI and its ilk in US markets could diminish over time, even as they continue to be used in offshore DeFi or as a niche hedge (e.g. in jurisdictions where access to fiat banking is limited). Overall, crypto-backed stablecoins face pressure to adapt or risk being cordoned off from the most liquid markets under the new regime.

Market Maker Implications

Market makers, firms that provide continuous buy/sell quotes and liquidity across crypto markets will play a pivotal role in the stablecoin liquidity transition. Under the GENIUS Act, their operating environment for stablecoins will change in several ways:

- Liquidity Fragmentation vs. Consolidation: In the short term, market makers may need to manage a fragmentation of liquidity. As noted, certain stablecoins (like USDT) could see reduced usage on US-based venues, whereas others (like USDC or new bank coins) gain traction. This means liquidity could splinter across different coins and jurisdictions. Market makers will adjust by reallocating capital and trading focus to the stablecoin tickers that remain permissible in the US. For instance, we may see USDC or a federally issued stablecoin become the dominant quote currency on US exchanges, while USDT liquidity concentrates on offshore platforms. Efficient market makers will arbitrage price discrepancies between these pools, helping prevent major dislocations between, say, USDC/USD and USDT/USD markets. In the long run, if the Act succeeds in consolidating trust around regulated stablecoins, overall liquidity could deepen. A more regulated, stablecoin ecosystem may attract new institutional participants (e.g. hedge funds, HFT firms, etc.) who were previously cautious, thus increasing the depth and stability of order books for compliant stablecoins.

- Regulatory Compliance and Constraints: Market makers themselves will need to navigate stricter compliance when dealing with stablecoins. Counterparty checks and KYC will become even more important. Since issuers must enforce blacklists and freeze illicit funds, a market maker must ensure it isn’t transacting with sanctioned or high-risk addresses to avoid having assets frozen mid-trade. This adds compliance overhead, for example, integrating on-chain analytics and whitelisting of “clean” wallets, but these practices are already familiar to large trading firms working in regulated environments. Additionally, any US-regulated market maker will be forbidden from treating unregulated stablecoins as cash equivalents in their accounting or collateral management. Thus, a firm can’t use (or accept) something like USDT or DAI as collateral for loans or margin on a US platform once the rules kick in. This constraint effectively forces liquidity providers to stick to approved stablecoins for any onshore operations. There may be an adjustment period where spreads on less-favoured stablecoins widen and market makers demand higher risk premiums to handle them. Over time, however, one can expect liquidity to concentrate where regulatory certainty is highest, simplifying compliance for market makers as well.

- New Opportunities via Institutional Stablecoins: The GENIUS Act is opening the door for large financial institutions to issue stablecoins, which in turn create new markets for liquidity. For example, if JP Morgan, Bank of America, or fintech consortium launch their dollar tokens, these assets will need active trading pairs and market making to be viable. A market maker could establish itself early as a primary liquidity provider for a new bank-backed stablecoin, benefiting from first-mover advantages. We are already seeing initiatives like WisdomTree’s USDW (a dollar stablecoin for tokenised assets) and Anchorage Digital’s USDᵗᵇ (a bank-issued stablecoin) emerge to comply with the Act. Each new stablecoin may initially suffer from shallow liquidity or price friction; market makers can earn significant fees by facilitating tighter spreads and arbitrage between these tokens and existing ones. Moreover, the Act’s legal clarity might allow traditional trading firms (which previously avoided crypto) to start market making in stablecoins, knowing they are dealing with regulated, non-securities assets. This broader participation can further professionalise and stabilise the stablecoin market.

- Use of Stablecoins in Settlements: With regulatory blessing, stablecoins could be more widely used in settlement and margining by clearing houses and brokers, which creates efficiency gains for market makers. Under prior uncertainty, US clearing firms were hesitant to accept stablecoins as collateral. The Act explicitly enables permitted stablecoins to serve as cash collateral in futures, swaps and other derivatives clearing, and as settlement assets in interbank payments. Once implemented, a market maker might post stablecoins to meet margin on a crypto futures trade or settle a trade after hours without waiting for wire transfers. The ability to seamlessly move stablecoin liquidity in and out of trading venues 24/7 is a boon. It reduces the friction and downtime associated with fiat banking hours. In essence, regulated stablecoins may become the “digital dollars” that grease the wheels of trading. Market makers could hold significant inventories of stablecoins with more confidence in their stability and acceptance. They will, however, monitor the health of each issuer (via monthly reserve reports and disclosures) and adjust their exposure if any red flags arise (e.g. an issuer’s reserves showing too much risk or a regulatory action against an issuer).

In summary, market makers will be both agents and beneficiaries of the GENIUS Act’s changes. In the near term, they must adapt to a shifting stablecoin menu and ensure rigorous compliance. Over the longer term, a well-regulated stablecoin environment should lead to greater liquidity, tighter spreads and new business lines (like supporting institutional tokenised money) for these liquidity providers. The Act’s prevention of runaway stablecoin risk (by mandating full reserves and oversight) also protects market makers from sudden stablecoin collapses that could freeze their capital (as happened with Terra’s implosion). Thus, from a market structure perspective, many anticipate a net positive effect on market integrity and liquidity, albeit with some adjustment costs along the way.

Global Outlook

Stablecoins are a global phenomenon, so US regulation will have international ripple effects. With the GENIUS Act, the United States joins a growing list of jurisdictions rolling out tailored stablecoin rules. The European Union’s MiCA framework (Markets in Crypto-Assets Regulation), which took effect in 2024, similarly requires stablecoin issuers in Europe to obtain licenses, maintain reserves and adhere to disclosure and prudential standards. MiCA caps large stablecoins’ volume in payments and mandates that euro-backed stablecoins are used for euro transactions, reflecting the EU’s cautious approach to not let foreign (USD) stablecoins dominate everyday commerce. Other regulators from Singapore to Japan have also acted: Singapore, via its Payment Services Act, licenses digital payment token issuers under clear guidelines, and Japan pioneered a law in 2023 that only banks and licensed trust companies can issue yen-pegged stablecoins. This global regulatory convergence means that in major financial centres, stablecoin issuers will face broadly similar expectations: full backing, fit-and-proper issuers, and oversight. For internationally active stablecoin projects, it won’t be feasible to comply in one jurisdiction and ignore another, they will need a strategy to satisfy multiple regulators or geo-fence their tokens to certain regions.

From a liquidity perspective, the GENIUS Act may further entrench the US dollar’s dominance in the digital asset economy. Already, about 90% of stablecoin value is tied to USD. With the US now actively supervising stablecoins, USD-backed tokens could become even more trusted globally, potentially outcompeting stablecoins pegged to other currencies. This raises interesting geopolitical questions. Some analysts (e.g. within the EU and developing countries) have voiced concern that widely adopted USD stablecoins could export U.S. monetary influence or pose “crypto-dollarization” risks to other economies.

Another global consideration is how unregulated stablecoins will find refuge outside the US framework. Tether’s strategy is a case in point, if it opts out of US compliance, it will concentrate on markets like Asia, Latin America, the Middle East and within the crypto-native community where users value its liquidity and may not face enforcement. Indeed, stablecoin adoption is high in regions with volatile local currencies or capital controls (e.g. USDT is popular in parts of Africa and South America as a dollar substitute). Those use-cases will persist. Countries that have not yet legislated stablecoin rules might become arenas for less-regulated stablecoins to circulate. However, as global standards crystallize and organizations like the Financial Stability Board (FSB) push for worldwide stablecoin principles, it will become harder for a large stablecoin to completely evade oversight. We can expect international coordination to increase. The GENIUS Act itself requires foreign issuers to meet “comparable” regulations; this creates an incentive for US allies and major economies to establish comparable regimes so that their companies can participate. Over time, a patchwork of bilateral agreements or mutual recognition could emerge, where a stablecoin licensed in Country X is approved for use in Country Y’s markets because both follow similar rules.

For global market makers and crypto firms, a more standardized regulatory environment for stablecoins is a double-edged sword. On one hand, it reduces regulatory arbitrage, the days of a stablecoin freely shopping for the least restrictive jurisdiction may be ending. On the other hand, greater certainty and uniformity can boost cross-border liquidity. Firms will know that a stablecoin coming from, say, a UK-licensed issuer or a Japanese bank, has a transparent reserve and compliance controls, making it safer to integrate into global trading and payment flows. This can expand the pool of “high-quality” stablecoins that traders are willing to use, beyond just the current incumbents.

In summary, the GENIUS Act positions the US as a leader in setting stablecoin norms, which is likely to spur a wave of international regulatory alignment.. The era of unchecked stablecoin growth is ending; a more governed era is beginning. For liquidity, this means short-term adjustments but potentially a more resilient and interconnected global stablecoin market in the years ahead, as multiple jurisdictions’ regulated stablecoins co-exist and even interoperate. The ultimate vision – if regulators and industry get it right, is a world where sending value is as trusted and easy as sending an email, with stablecoins in various currencies providing the digital cash to do so, without the wild west risks of the past.

Conclusion

The passage of the GENIUS Act marks a turning point for stablecoins and their role in the crypto market. By crafting a detailed regulatory framework, the US government is signalling that stablecoins have graduated from an experimental tool to a matter of national financial infrastructure. The Act brings stablecoins under the umbrella of bank-like regulation, demanding sound reserves, honest operations and robust compliance. This will undoubtedly constrain certain practices and require adjustments by issuers and traders – gone are the days of unchecked issuance and opaque reserves. Yet, it also paves the way for much greater integration between crypto liquidity and traditional finance. A well-regulated stablecoin can be the bridge asset connecting these worlds, facilitating everything from everyday payments to settlement of tokenised securities.

From a market maker’s perspective, the new era will involve adaptation to stricter rules but also offers fresh opportunities. Liquidity providers will gravitate toward the most compliant and liquid coins, and in doing so, help reinforce their stability. In time, we expect fewer but more robust stablecoins, supported by both crypto-native firms and incumbents, driving deeper liquidity in trading venues. The ability to reliably move large sums on-chain in a regulated manner could unlock new trading strategies and 24/7 financial services that were previously hampered by fiat frictions.

Internationally, the GENIUS Act’s influence will be felt as countries either embrace similar standards or risk seeing stablecoin activity relocate. The competitive advantage may tilt towards jurisdictions that provide a clear, safe harbour for stablecoin innovation. For the US, taking the lead with this Act could solidify the dollar’s digital dominance – a strategic outcome that the authors of the bill no doubt intended.

In conclusion, the “new era of stablecoin liquidity” is one of maturation. The free-for-all phase is ending; a phase of regulated growth and technical refinement is beginning. Stakeholders across the board, issuers, exchanges, market makers, and users, will need to collaborate within the guidelines to realise the benefits. If successful, stablecoins could truly become the efficient, globally trusted liquidity instruments that early adopters envisioned, supporting innovations in payments and finance on a much larger scale. The GENIUS Act is a bold step in that direction, balancing innovation with safeguards. As the rules are implemented in the coming months, we will gain an even clearer picture of how stablecoin liquidity evolves. For now, what’s certain is that stablecoins are no longer operating in the shadows; they have entered the arena of mainstream finance, with all the responsibilities that implies. The crypto markets will be watching closely as this new chapter unfolds, adjusting strategies and seizing opportunities in a landscape defined as much by technology as by law.

Further Reading

- The analysis above references the GENIUS Act’s text and summaries:

congress.gov - Industry legal analyses:

sidley.com - U.S. congressional records

congress.gov - Commentary from market experts and news outlets (CoinDesk, Cointelegraph, Chainalysis, ICBA) to provide a comprehensive, up-to-date picture of the legislation’s impact.

All information is sourced from public documents and reports as of July 2025.

Contact Us

We are always open to discussing new ideas. Do reach out if you are an exchange or a project looking for liquidity; an algorithmic trader or a software developer looking to improve the markets with us or just have a great idea you can’t wait to share with us!